Accounting is the portrayal of business. It is often regarded as the language also. It is the process of recording, summarizing, analyzing, and reporting financial transactions of a business or organization.

Accounting provides crucial information about the financial position and performance of a business. It helps in budgeting, planning and decision-making for the future.

The Accounting Equation: Assets = Liabilities + Equity.

Assets: Assets are resources owned by a person, business, or any entity that have economic value and can be converted into cash or cash equivalent. Examples include cash and cash equivalents, investments, property plant & equipment, Inventory, accounts receivable, and intellectual property.

Liabilities: Liabilities represent debts or obligations owned by an individual, company, or any entity to other parties. They are obligations to transfer economic benefits, such as money, goods, or services. Examples include accounts payable, loans, leases, income tax payable, and accrued expenses.

Equity: Equity in finance and accounting represents the residual interest in an entity’s assets after deducting liabilities. It is essentially the ownership interest in a business or assets. Examples include common stock, preferred stock, retained earnings, contributed surplus, additional paid-in capital, treasury stock, dividends, and other comprehensive income (OCI).

Types of Accounts:

There are several types of accounts used in accounting to organize and track financial transactions. Here are the main types:

1. Personal:

♦ Natural

♦ Artificial

♦ Representative

Rules: Receiver – Debit, Giver – Credit.

2. Real:

♦ Tangible

♦ Intangible

Rules: Comes into business – Debit, Goes out of business – Credit.

3. Nominal:

Rules: Expenses or Losses – Debit, Income or Gains – Credit.

Types of Accounting:

Main eight (8) types of accounting are:

Financial Accounting: Financial Accounting is a branch of accounting that focuses on the preparation of financial statements. Its primary objective is to provide accurate and reliable information about a business entity’s financial position, performance and cash flows.

Managerial Accounting: Managerial Accounting is the process of identifying, measuring, analyzing, interpreting and communicating financial information to assist managers in making organizational decisions. It focuses on internal reporting and is used by managers to plan, control, and optimize business operations. Managerial accountants often deal with cost analysis, budgeting, forecasting, performance evaluation, and strategic planning.

Cost Accounting: Cost Accounting is a branch of managerial accounting that focuses specifically on identifying, measuring, analyzing, and allocating costs associated with producing goods or services.

Tax Accounting: Tax Accounting involves the preparation, analysis, and filling of tax returns and compliance with tax laws and regulations. It focuses on optimizing tax liabilities and maximizing tax benefits for individuals or businesses.

Auditing: Auditing is the systematic examination and evaluation of financial records, transactions, and operations of an organization to ensure accuracy, compliance with laws and regulations, and adherence to established internal controls. The primary purpose of auditing is to assure stakeholders, such as shareholders, investors, creditors, and regulators, about the reliability and integrity of the financial information presented by the entity. Auditors, typically independent third parties, review financial statements, assess the effectiveness of internal controls, and report any findings or discrepancies. The audit process helps detect errors, fraud, or misstatements and provides recommendations for improvement. An auditor usually concludes whether the financial statements ‘give a true and fair view’.

Forensic Accounting: Forensic accounting involves the application of accounting principles, investigative techniques, and legal concepts to analyze financial information for use in legal proceedings, dispute resolution, or fraud investigations. Forensic accountants utilize their accounting expertise to uncover financial irregularities, such as embezzlement, money laundering, or fraudulent financial reporting, and provide evidence that can be used in litigation or criminal proceedings. They often work closely with law enforcement agencies, attorneys, and other professionals to uncover, document, and present financial evidence in a court of law.

Governmental Accounting: Governmental accounting refers to the accounting practices and standards used by governmental entities, such as federal, state, and local governments, as well as agencies, municipalities, and other public sector organizations. It encompasses the recording, reporting, and analyzing financial transactions and activities specific to government operations. Governmental accounting often follows specialized accounting principles and standards tailored to the unique needs and requirements of the public sector, such as fund accounting, budgetary accounting, and compliance reporting. It aims to provide transparency, accountability, and stewardship of public funds while meeting legal and regulatory obligations.

International Accounting: International accounting refers to the accounting practices and standards used by multinational corporations and organizations operating in multiple countries. It involves preparing, presenting, and interpreting financial information by global accounting principles and standards, such as the International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP) in the United States. International accounting addresses the challenges of dealing with diverse currencies, regulatory environments, taxation systems, and cultural differences across different jurisdictions. It aims to provide consistency and comparability of financial information for stakeholders across borders and facilitate decision-making in an increasingly globalized business environment.

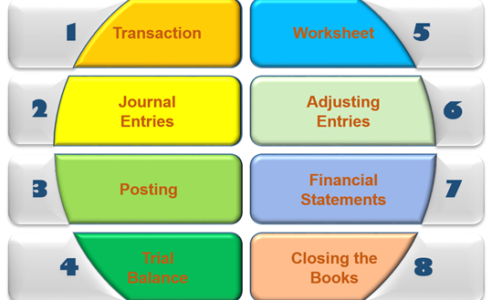

Accounting Cycle: